The recovery rally in equities over the past few months has brought into focus a topic that many investors argue about passionately – namely, which investment style is more attractive, value or growth?

In recent months, so-called value stocks have risen more than growth stocks, while over the past few years growth stocks have outperformed value stocks, in some cases significantly. What is behind this development?

To begin the discussion, let’s first shed some light on this classification.

Growth stocks are stocks that show high earnings or sales growth and/or a high price/earnings ratio. The business model of the underlying company or sector allows for high growth, and business performance is usually less dependent on changes in economic growth. Conversely, value stocks benefit more than average from economic growth and therefore usually have a stronger cyclical component. They are typically mature companies, have steady growth rates, and exhibit relatively stable sales and earnings. In addition, they tend to offer more favourable valuations than their growth counterparts.

A direct performance comparison between value and growth stocks can be misleading, as the two categories sometimes have different risk levels. Growth stocks often fluctuate more strongly.

An allocation strategy based purely on the classification between growth and value entails risks. Any investment decision must be supplemented with further qualitative considerations regarding entrepreneurial perspectives.

During the crisis, many business models belonging to the growth category benefited greatly, whereas companies in the value category were sometimes heavily burdened. The post-Covid recovery is now partially reversing this trend, as developments such as infrastructure investment programmes often have a stronger positive impact on companies in the value category.

However, investors should also not neglect the fact that many companies in the growth category are not small start-ups with uncertain prospects, but sometimes giants with very promising business models. As is so often the case, the truth likely lies in the middle, so a sensible mix of companies from both categories should be purposeful. In any case, however, attention should be paid to the quality and plausibility of expectations.

Learn more reading our May outlook by UniCredit Wealth Management

CHART

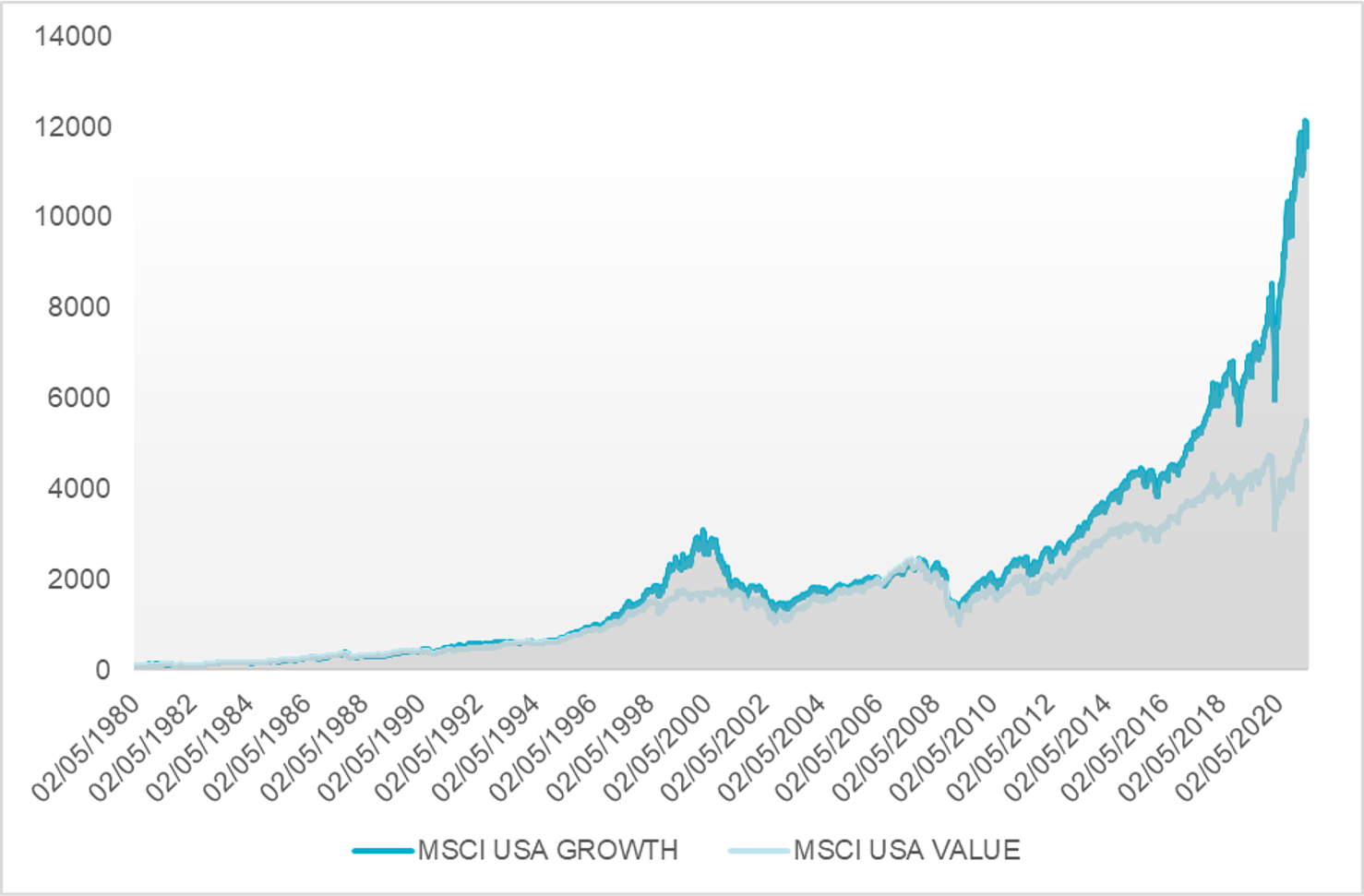

Market capitalisation MSCI USA Growth and MSCI USA Value.